When it comes to BOI reporting, navigating complex ownership structures can be challenging. Understanding and accurately disclosing individuals with a significant stake in your company is crucial for compliance. In this guide, we’ll provide a streamlined approach to handling complexity in BOI reporting while incorporating essential keywords for SEO.

Understanding & Navigating Complex Ownership Structures

BOI reporting revolves around identifying individuals who own, control, or significantly influence a business. In complex ownership structures, these individuals may be concealed behind layers of entities, trusts, or arrangements. Unraveling this web is essential for BOI compliance.

Determining if a company must disclose beneficial ownership details can become complex when ownership structures involve multiple layers or entities.

Companies with many owners spread across different entities or trusts may not have any single individual meeting the 25% ownership threshold. However, if these owners act together, they could exert significant control, triggering reporting requirements. It is essential to scrutinize ownership stakes and decision-making authority in such cases.

Multiple Layers of Ownership

When a trust or a company owns another company, determining the ultimate beneficial owner (UBO) requires a closer examination of the ownership structure. The UBO is the individual who ultimately controls or benefits from the company, despite any layers of trusts or corporate entities in place. This often involves tracing ownership up through the parent company or trust to identify the person who holds significant control or economic interest.

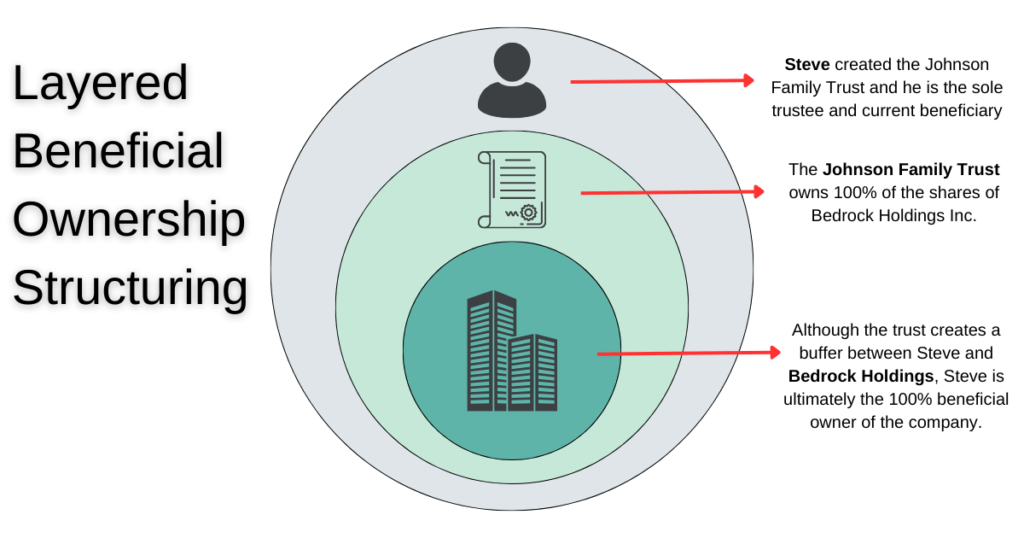

The illustration depicts a nested structure of corporate ownership with three layers:

- The innermost circle represents Bedrock Holdings Inc., the operating company that generates revenue and is responsible for reporting its beneficial owners.

- The middle circle represents the Johnson Family Trust, which owns Bedrock Holdings Inc.

- The outermost circle represents Steve, who is both the trustee and beneficiary of the Johnson Family Trust.

This layered structure demonstrates how Steve indirectly controls Bedrock Holdings Inc. through the intermediary entity of the Johnson Family Trust. As a result, Steve is identified as the Ultimate Beneficial Owner (UBO) of Bedrock Holdings Inc.

In this scenario, Steve would be reported as the UBO on the Beneficial Ownership Information (BOI) report for Bedrock Holdings Inc. This is because Steve, as both the trustee and beneficiary of the Johnson Family Trust, exercises ultimate control over the company, despite not directly owning it.

Challenges in Determining All Beneficial Owners

Determining all beneficial owners can become challenging when there are multiple owners and layers of different corporations involved in owning a company. In such complex structures, ownership stakes can be spread across various entities, making it difficult to pinpoint who ultimately controls or benefits from the company. Typically, individuals owning less than 25% are not considered beneficial owners, while those owning more than 25% are identified as beneficial owners.

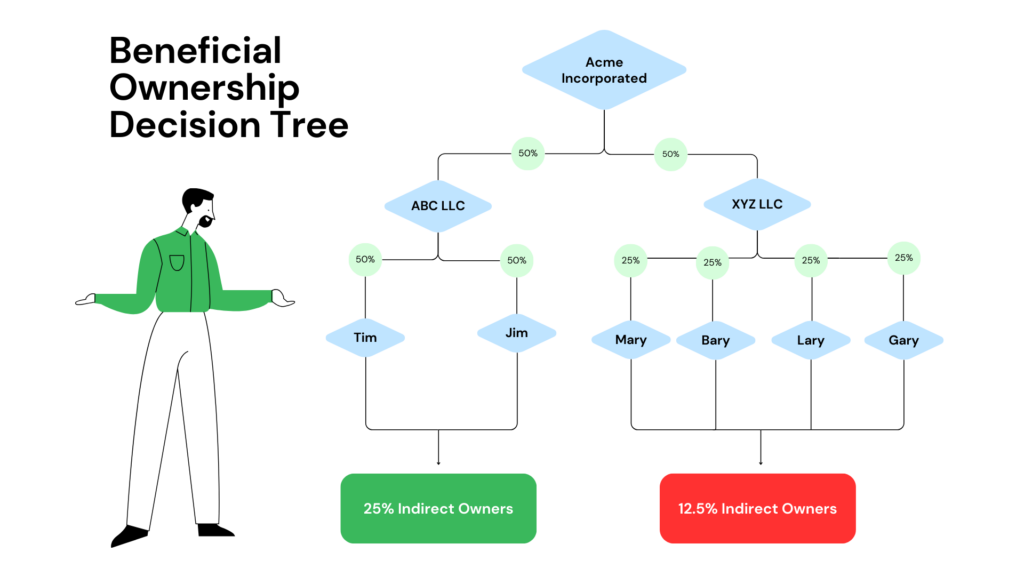

In the example above, Tim and Jim each own 50% of ABC LLC, which in turn owns 50% of Acme Incorporated. Mary, Bary, Lary, and Gary each own 25% of XYZ LLC, which owns the other 50% of Acme Incorporated.

Assuming none of the owners in XYZ LLC are considered control persons of Acme, they would not need to be reported as beneficial owners of Acme, as their individual ownership in Acme is only 12.5%, below the 25% threshold. However, XYZ LLC would still need to report each of them as beneficial owners of as they all own 25% of that company.

Tim and Jim reach the 25% ownership threshold for both ABC LLC and Acme Incorporated and therefore would be reported as beneficial owners for both companies.

What if there isn’t a 25% Beneficial Owner?

If no individual within a company, or from the parent company, owns 25% or more of the entity, at least one person must be designated as the “control person” and listed as a beneficial owner in the Beneficial Ownership Information Report (BOIR). The control person is typically an individual with significant authority over the entity’s operations, such as a senior officer (e.g., CEO, CFO, or general manager), and is required to fulfill the reporting obligations for compliance.

Simplified Steps to Handle Complexity

1. Identify All Ownership Layers

For companies with multi-layered ownership structures involving other entities or trusts, it is crucial to trace the ownership trail to identify the ultimate individual beneficial owners. This may involve “piercing the corporate veil” by looking through multiple layers of ownership to determine the individuals who ultimately own or control the company.

It may help to map out your entire ownership structure, including indirect involvements. Trace back to the natural persons who ultimately own or control the business.

2. Assess Ownership Stakes and Control

Even if no single individual meets the 25% ownership threshold for reporting, companies should carefully analyze ownership stakes and decision-making authority. If multiple owners are working in concert and have significant control over the company, they may still need to be reported as beneficial owners.

3. Maintain Comprehensive Records

Maintaining comprehensive and up-to-date records of ownership information, including details on individuals, entities, and ownership percentages, can be invaluable. These records can serve as a reference point for BOI reporting and help ensure compliance with evolving regulations.

4. Leverage FinCEN BOI Filing as a Resource

The tools and resources on FinCENBOIFiling.com are available to everyone, providing valuable assistance in determining your reporting requirements.

To find out quickly if you are required to file a BOI report for your business, check out our free 2-minute Eligibility Quiz.

Common Pitfalls to Avoid

- Ignoring Indirect Ownership: Include all indirect paths, as even minority stakeholders in intermediary entities can hold substantial control.

- Avoiding Assumptions: Each complex structure is unique, requiring a tailored approach.

- Procrastinating Reporting: Start early to allow time for unraveling complexities.

Complex Ownership Structure Summarized

Navigating complex ownership structures in BOI reporting is challenging but manageable with a systematic approach, expertise, and the right tools. FinCEN BOI Filing offers solutions for simplified reporting, ensuring BOI compliance. Thoroughness, accuracy, and staying informed are key to managing BOI complexities.

العربية

العربية Հայերեն

Հայերեն 简体中文

简体中文 Nederlands

Nederlands English

English Filipino

Filipino Français

Français Deutsch

Deutsch Kreyol ayisyen

Kreyol ayisyen हिन्दी

हिन्दी Italiano

Italiano 한국어

한국어 پښتو

پښتو فارسی

فارسی Português

Português ਪੰਜਾਬੀ

ਪੰਜਾਬੀ Русский

Русский Español

Español Українська

Українська اردو

اردو Tiếng Việt

Tiếng Việt